By Gavin Bridge, Durham University, Alexander Dodge, NTNU, James Marriott, Platform-London, and Nana de Graaff, VU-Amsterdam.

Fending off criticism of record profits, BP has spent big on an advertising campaign “Backing Britain: Delivering Homegrown Energy”. It is not alone in asserting corporate ties to national territory and the value of domestic oil and gas extraction. The new Prime Minister has promised to accelerate oil and gas investment in the North Sea as a response to the cost-of-living crisis. But appeals for ‘homegrown hydrocarbons’ simplify the complex international relations of production, trade and profit that characterise UK oil and gas. Expanding UK oil and gas production will not reduce energy prices.

The cost-of-living crisis has dominated the UK political landscape this summer. As prices for natural gas rose to record highs, household energy bills were projected to top £4200 per year for an average home. So, when BP issued its quarterly financial report in August, there was more than the usual frisson associated with the reporting of oil company profits. The firm, which has its head office in London, made a profit of US$ 9.3 billion (£7.6 billion) in the second quarter (the highest for 14 years) and said it would channel much of this surplus cash to shareholders, raising its dividend and buying back blocks of shares. BP is not alone: other international oil and gas companies active in the UK, like Shell, Total and Neptune, have also reported record earnings.

As shareholders of oil and gas companies extract an ‘upside’ from the UK’s growing cost of living crisis, there have been calls to tighten the energy profits levy – i.e. the ‘windfall tax’ introduced in May this year, payable by companies that extract oil and gas in the UK – and use the money to establish a social energy tariff, invest in household insulation, and bring the country’s energy supply companies into national ownership. Behind such calls are fundamentally geographical questions – about the ties of global corporations to national territory, the place of hydrocarbon extraction in net zero transition, and the patterns of trade by which the UK balances demand and supply for oil and gas.

Such questions form the subtext of BP’s current national advertising campaign, which places the words ‘Backing Britain: delivering homegrown energy” in green letters on a map of the UK. The company boosted spending on these adverts ahead of the windfall tax announcement in May, and again around the August quarterly results. In them, BP commits to invest up to £18 billion in UK energy projects by 2030 to provide “the home-grown energy security the UK needs while helping the country to achieve its next zero ambitions.” Text and graphics in these adverts articulate strong ties between company and country – a sense of mutual dependence supported by a shared history – with the company’s oil and gas operations described as “bringing a reliable flow of energy from deep below the waters of the North Sea for 60 years and supporting thousands of jobs.”

Contending geographies of oil and gas

What is at stake in these geographical claims? Our research with colleagues into Networks, Territory and Transformation in the UK Oil Sector is examining the evolving connections – and fraying ties – between international oil and gas firms and the UK. BP’s name-plate association with the country and history as a ‘national champion’ make it an interesting case, and our recent findings provide context for August’s quarterly results and the ‘Backing Britain’ campaign. Both come at a time when the company’s oil and gas footprint in the UK has been shrinking and its centre of gravity shifting elsewhere. BP’s appeal to a geography of ‘home-grown energy’ is now being taken up more widely, in calls by industry and government to address the cost-of-living crisis by expanding the production of oil and gas in the UK. But the implied equation of more UK production with lower UK prices rests on a ‘naïve geography’ of supply and demand, and does not reflect the international political economy of production, trade and profit that has evolved around the UK oil and gas sector.

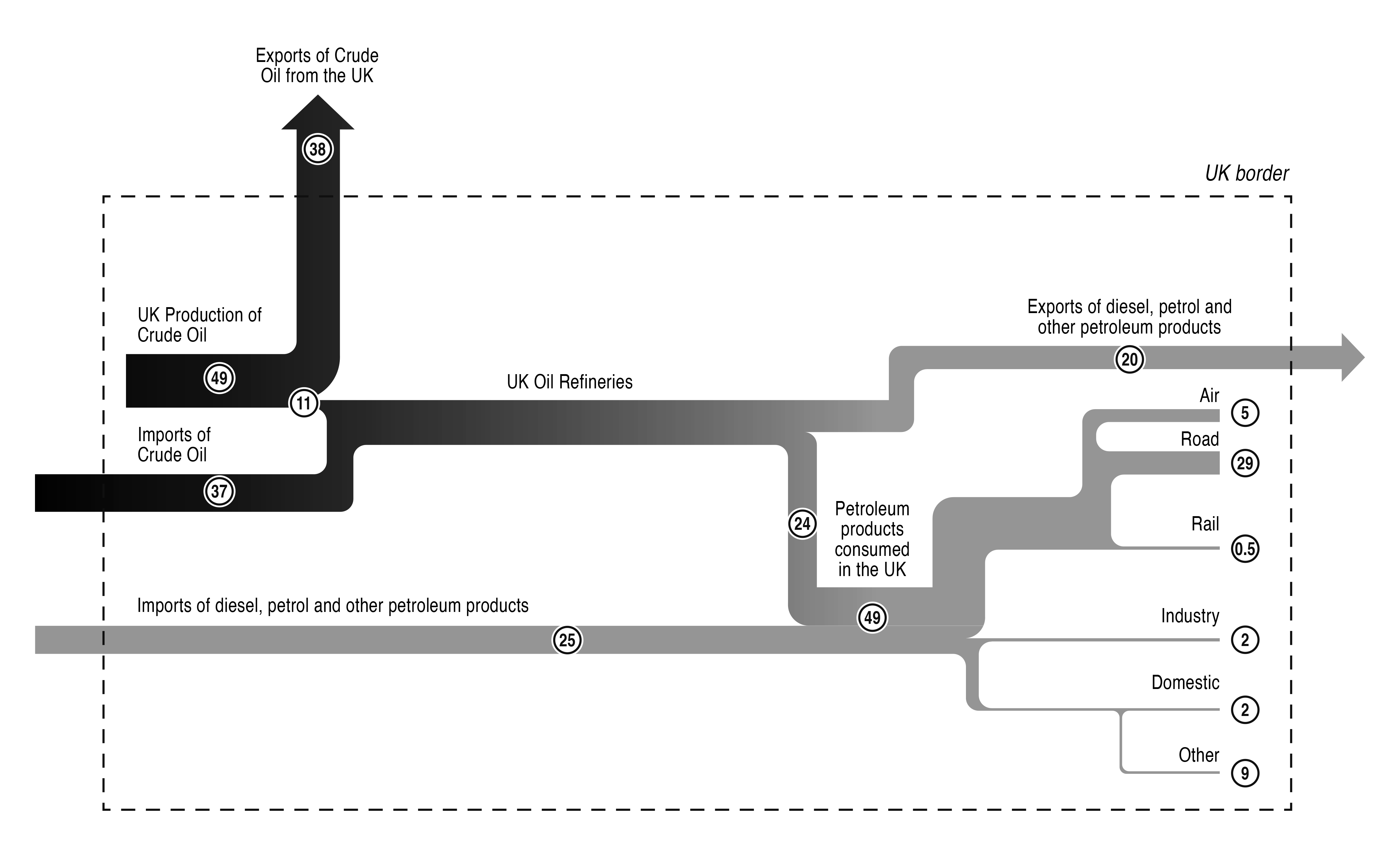

Most ‘home’ oil production is exported

Offshore production of hydrocarbons – and onshore demand – are less tightly connected than one might think. Take oil, for example (Figure 1). The six major oil refineries in the UK are fed mainly by distant sources of crude with ‘home-grown’ production supplying only one in seven barrels (14%) in 2021. There is no requirement that oil produced from UK territory flows to UK consumers and most of it does not: in 2020 over a quarter of UK oil production was destined to fuel cars in China, rather than supplying the forecourts of local petrol stations, while nearly half of UK crude exports are destined for the Netherlands. When you fill up at the pump, there’s a good chance the fuel was imported (Russia supplied around a third of the UK’s diesel imports in 2021). And, even if your petrol or diesel came from a UK oil refinery, it is more likely to be based on crude from Norway or the United States than from the North Sea. The situation for gas is different – pipelines bring the gas onshore where it is fed into the national transmission network – although the UK’s connectivity to the continent and reliance on imports mean physical supply security does not mean security of price.

Fraying ties – corporate focus shifting elsewhere

Like many of the companies associated with the historic development of the North Sea, BP’s footprint as a hydrocarbon producer in the UK has shrunk significantly. The company has disposed its UK refining capacity, chemical production plants, offshore pipelines, and fuel import depots and, facing strong civil society pressure, has also been winding up sponsorship of the cultural sector. BP has sold off historically significant North Sea assets, including the large Forties field that at its peak produced over half a million barrels per day. It also sold gas fields in the southern North Sea and one of the largest onshore oil operations in Europe (Wytch Farm in Dorset) in the wake of Deepwater Horizon. When measured by oil & gas production, the company slipped from top spot in 2000 (accounting for around 15% of UK output) to third place in 2020 (less than 9% of production) as other companies have taken its place.

BP maintains a substantial foothold in the North Sea, with the largest recoverable oil and gas resources of all companies operating on the UK Continental Shelf. Recent investment has focussed on the central North Sea (e.g. around the ETAP hub) and West of Shetland (e.g. Clair and Schiehallion fields). Nonetheless, the significance of the UK within BP’s oil and gas portfolio has declined. Today the UK accounts for less than 1/20th of the company’s oil output, compared to around a quarter in 2000. Similarly, the UK accounted for quarter of the company’s crude oil reserves in 2000 (and about an eighth of its gas) but by 2020 this had fallen in both absolute and relative terms, representing only 3% of the company’s reserves of crude (and less than 1% of gas). The recoverable resources BP holds in the UK are a fraction (3%) of its worldwide holdings: for example, less than a sixth of what it holds in the US and smaller than its position in Azerbaijan, Senegal and Mauritania.

International markets drive price, not local production

Like other oil and gas producers, BPs activities in the North Sea do not have much impact on the prices UK consumers pay for their petrol or heating bills. When crude oil is traded, it is valued against international benchmark prices such as Brent Crude. Although Brent refers to a grade of oil extracted from the North Sea it is a waterborne crude that can be shipped and sold anywhere around the world, so its price is set by global markets. Prices for natural gas are similarly determined by international trading, so that ‘home-grown’ gas extracted in the UK is sold at prices that reflect those in Europe and Asia. Furthermore, energy prices are determined not only by ‘market fundamentals’ of physical supply and demand but are also driven by speculative trading.

BP: Less British, More American?

The directors of oil and gas firms influence corporate culture and governance structures, and shape decisions around investment and divestment strategies in places such as the UK. Directors do not act in a social vacuum, however, but are connected through personal and professional affiliations to wider networks. These social networks serve as important channels of communication among directors and can facilitate formation of a common worldview. Our research shows that corporate Board-level ties between BP directors and other firms headquartered in the UK have dropped significantly since the 2000s, declining from 55% to 32% as a proportion of total ties (Figure 2). At the same time, the corporate social networks linking BP to US headquartered firms have increased proportionally over time to outnumber UK ties. Given the significant influence of Board directors and the corporate networks in which they are embedded on corporate strategy, this suggests BPs affiliation with the UK is less significant than its ties to the US.

Conclusion

As the UK’s cost of living crisis intensifies, there are growing calls to boost domestic production of oil and gas. The new Prime Minister is among them, announcing a drive to accelerate licensing, investment and production for oil and gas and an ending of the moratorium on fracking. The UK has substantial hydrocarbon production already – the second largest in Europe, after Norway – but this has provided the UK little protection, as households and businesses are paying similar or even higher prices for energy than countries with no oil and gas production. Oil and gas extraction in the UK is integrated with global markets. So too is the domestic consumption of oil and gas products. These interconnections mean that prices British consumers pay for energy are not determined by how much oil or gas is produced on the UK Continental Shelf, but by trading on international exchanges. This is as true for ‘home-grown’ oil and gas as it is for imports as, unlike some other countries, there are no domestic market obligations requiring UK oil and gas flow into the UK and/or reach British consumers at a preferential price. The integrated, international geographies of UK oil and gas challenge claims that boosting extraction at home will solve a cost-of-living problem. They also highlight how the UK footprint of an ostensibly ‘British’ company like BP has shrunk over time for its core business of oil and gas, and the diminishing role of UK assets in the company’s global portfolio. It is in the context of these fraying ties between company and country, rather than the immediate issue of record quarterly profits, that campaigns like ‘Backing Britain’ should be understood.

About the authors: Gavin Bridge is Professor of Economic Geography at Durham University. Alexander Dodge is an Associate Professor in the Department of Geography at NTNU. James Marriott is with Platform, London and is co-author of Crude Britannia. Nana de Graaff is an Associate Professor in the Department of Political Science at VU Amsterdam.

The research reported on here is undertaken as part of Fraying Ties? Networks, Territory and Transformation in the UK Oil Sector (ES/S011080/1). The support of the Economic and Social Research Council (UK) is gratefully acknowledged. Fraying Ties is an interdisciplinary research collaboration, and the authors acknowledge—with gratitude—the expertise, insight and support of other members of the project team: William Otchere-Darko, Tiago Teixeira and Gisa Weszkalnys. We thank Chris Orton at Durham University for design work on Figure 1 and Figure 2, Thomas Janssen at VU University for his assistance with data analysis behind Figure 2, and Mike Bradshaw for comments on an earlier draft. Thanking the above implies no responsibility for the arguments or content which are those of the authors alone. This blog draws in part on the following piece of recently published research: Bridge, G. and A. Dodge. 2022. Regional assets and network switching: shifting geographies of ownership, control and capital in UK offshore oil. Cambridge Journal of Regions, Economy and Society 15: 367–388.

The cover image for this post has been provided by the authors.

Suggested further reading

Bridge, G. and A. Dodge. (2022). Regional assets and network switching: Shifting geographies of ownership, control and capital in UK offshore oil. Cambridge Journal of Regions, Economy and Society https://doi.org/10.1093/cjres/rsac016

Bradshaw, M.J. (2010), Global energy dilemmas: a geographical perspective. Geographical Journal. https://doi.org/10.1111/j.1475-4959.2010.00375.x

Bridge, G. and Wood, A. (2005), Geographies of knowledge, practices of globalization: learning from the oil exploration and production industry. Area https://doi.org/10.1111/j.1475-4762.2005.00622.x

De Graaff, N., (2011). A global energy network? The expansion and integration of non‐triad national oil companies. Global Networks https://doi.org/10.1111/j.1471-0374.2011.00320.x

Marriott, J and T. Macalister (2021) Crude Britannia: how oil shaped a nation. Pluto Press.

| How to cite: Bridge, G., Dodge, A., Marriott, J., & de Graaff, N. (2022, 26 September). ‘Backing Britain’: Soaring energy prices – and record profits – are driving global energy companies like BP to wrap themselves in the national flag. What’s at stake in these geographical claims? Geography Directions https://doi.org/10.55203/JOFH1925 |

I love the way you talked about The topic