By Mike Stephenson, British Geological Survey, UK

In the UK, industry accounts for a quarter of greenhouse gas emissions with most coming from a few energy intensive industries in tight geographical clusters, like Humberside and Grangemouth. It’s the same story across the developed world, and in the emerging economies new clusters of manufacturing and industry are set to develop and grow. The way that these industrialised areas decarbonise will be crucial to the environment, to climate change, and staying within the ambitions of the Paris agreement.

What we might call the ‘carbonisation’ of the industrial revolution (as opposed to ‘decarbonisation’) was stimulated by the distribution of geological resources like iron ore, high calorific coal and limestone so that areas like the north of England could rapidly industrialise in the 18th Century. In the same way, rock properties are today influencing the positions of modern industrial decarbonisation clusters, for example availability of CO2 geological storage space for fossil fuel power stations and industries or for hydrogen manufacture from steam methane reformation. Other underground technologies needed include hydrogen storage, compressed energy storage and heat storage.

The advantage for emerging economies as they develop their industrial clusters is that they can leapfrog some of the retrofits associated with the legacy technology of older clusters, and design decarbonised systems from scratch. These will deliver manufacturing capability and growth but also maintain a liveable environment and work towards climate abatement.

But where will these fit-for-purpose clusters be, and what will they look like in the emerging economies in Africa and Asia? What will be the effects of the COVID global downturn on decarbonisation clusters?

Cluster anatomy

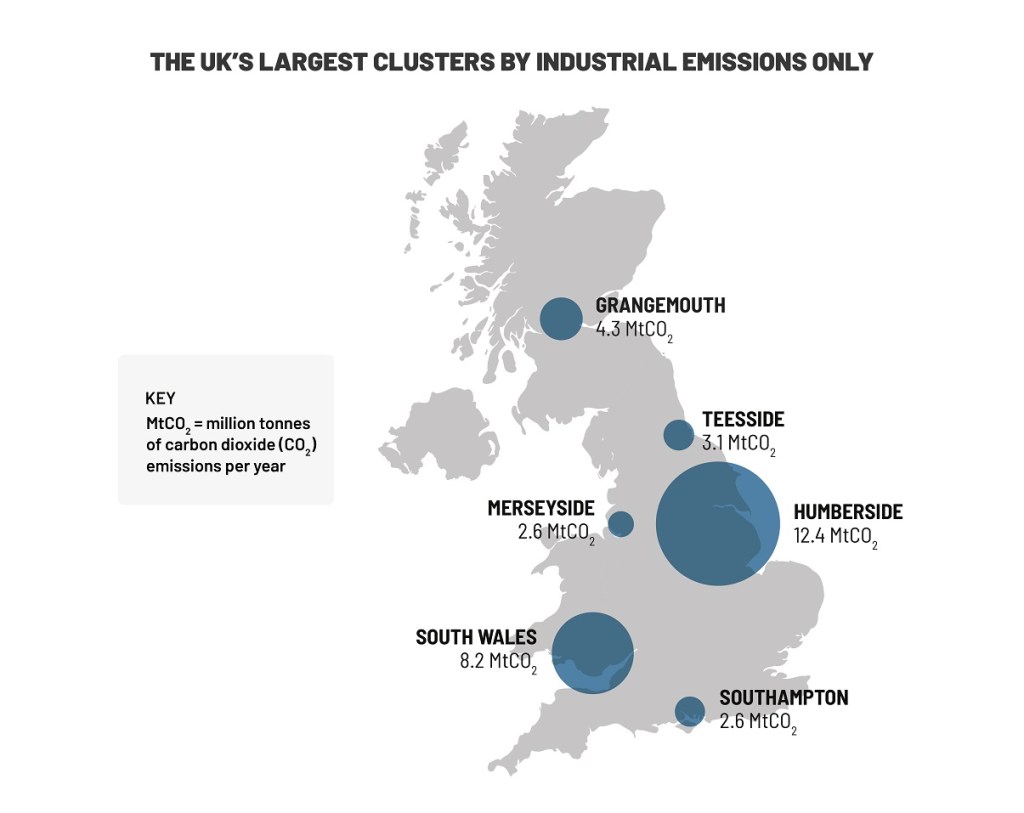

Industrial decarbonisation clusters are a big part of the UK government’s Industrial Strategy, the Industrial Clusters Mission and the newly established Industrial Decarbonisation Research and Innovation Centre (IDRIC). The aim of the Industrial Clusters Mission is to create a net zero industrial cluster in the UK by 2040, by attracting investors and innovators and getting big emitters in geographical proximity to work together. In the UK, the biggest clusters by emissions are Humberside (12.4 MtCO2/yr), South Wales (8.2 MtCO2/yr) and Grangemouth (4.3 MtCO2/yr). The clusters contain mixtures of industries often linked through supply chains, common fuels and common infrastructure – but also now linked by the need to decarbonise.

An example is in the northwest of England around the Mersey estuary. Here big industrial gas users, fossil fuel power stations, refineries and offshore gas field operators are joining forces and with the help of local and central government are working towards a hydrogen economy that sees hydrogen buses on the roads, hydrogen trains, and hydrogen as a fuel for industry and power.

Clusters like this rely on an ‘industrial ecology’ but also on the right geological conditions. The obvious geological requirement in the UK and many other industrial nations with incumbent fossil fuel usage is geological space for CO2. The UK has benefited from numerous studies of offshore CO2 storage space such that now a detailed database, CO2Stored, hosted by the British Geological Survey, allows planners a first pass look at candidate underground stores. Other geological features needed in a cluster are storage space for hydrogen for seasonal and shorter cycle storage. The northwest cluster has CO2 storage space in soon-to-be-decommissioned gas fields in nearby Morecambe Bay, hydrogen storage space in salt caverns in Cheshire – and big users of industrial fuel that would be better provided in the form of hydrogen rather than natural gas.

Where decarbonisation really matters…

But more than 90% of energy demand growth between now and 2050 will take place outside the OECD countries and there is a continuing need expressed through the UN’s Sustainable Development Goal 7 to improve energy access to the poorest people.

In emerging economies in Africa and Asia, development corridors reveal the rapid growth of manufacturing, transport routes, mineral and hydrocarbon development. Examples of corridors in East Africa include the ‘northern corridor’ that loops around Lake Victoria, and the Nacala, Beira and Maputo corridors in Mozambique. East Africa’s population is forecast to grow from about 300 million today to 800 million by 2060 and 1150 million by 2090, and many people will reside in growing or new cities and rise in living standards and increase in population will increase energy demand, some of which may be satisfied by fossil fuels, though big increases in solar PV are likely too. New large fossil fuel finds in East Africa, for example coal around Tete in Mozambique and offshore gas in Mozambique and Tanzania mean that fuels will be available not only for home consumption but also for export.

Obviously the largescale take-up and use of fossil fuels would be a challenge for climate change targets and this highlights the importance of the emerging economies in reaching the Paris goals. Fossil fuel exploitation in developing countries has also not always lead to equitable development. But more sustainable use of fossil fuels within clusters is possible, and not just through CCS on fossil fuel power stations and industry. The co-occurrence of cheap solar, hydroelectricity and abundant natural gas could present an opportunity to develop both ‘green’ hydrogen where the gas is made through electrolysis, and ‘blue’ hydrogen where it is made through breaking down methane with geological disposal of the CO2 by-product. The IEA considers East Africa to have the potential to produce enough hydrogen for cheap manufacturing, low CO2 intensity steel production and perhaps processing and manufacturing of batteries with Africa’s abundant resources of critical metals like cobalt and tantalum. Hydrogen fuel cells could also be used for off-grid and back-up power for renewables intermittency. The IEA also sees a significant role for volcanically-sourced geothermal energy, particularly in Kenya.

But to be sure of the geology, systematic surveys of this volcanic geothermal, but also the potential for carbon dioxide storage and hydrogen will have to be done. Subsurface rocks will have to be seen rather differently – instead of containers from which materials are extracted, they should be regarded as containers for storage or disposal. At present, no systematic surveys for hydrogen storage have been completed in East Africa or elsewhere in Africa and knowledge of CO2 storage potential is patchy.

Virus effects

What will be the likely effects of COVID-19 on decarbonisation clusters? A recent IEA report predicts that global energy demand will fall by 6% in 2020. Low demand and price wars have already lowered oil, gas and coal prices. In frontier fossil fuel areas, these low prices may make production uneconomic which could hasten transition to full renewables. Slightly higher prices could undercut renewables though. The incumbency and lock-in of hydrocarbon energy infrastructure may also make a substantial renewables transition difficult even if the cost of production of renewable electricity is lower than that of fossil-fuelled electricity. Problems with very high renewable electricity production would include intermittency, the investment needed in long-range transmission of energy to combat intermittency, and the size of renewable infrastructure needed for modern and fast growing economies.

The development of clusters – of whatever flavour – will require significant investment, not only from industry but also from governments. But it may be that the outbreak, though terrible for the health of the population and economy, has changed attitudes. To get through the pandemic, governments have intervened financially, and populations have adapted to lock-in. In the UK, public money from the Industrial Strategy fund aims to address market failures and technical pinch points to get decarbonisation clusters projects past their ‘activation energy’ and moving under commercial momentum.

But technologies like CCS still don’t have a clear long term funding mechanism beyond infrastructure development and might benefit from the kind of financial intervention that governments have taken during the pandemic. After COVID, populations might be more willing to pay more for electricity and to bear the cost of intelligent investment in low carbon energy. It’s difficult to be certain. One thing is for sure, for all the horror that COVID has brought, it may make us better at dealing with big challenges, including the climate-energy challenge.

About the author: Mike Stephenson is Executive Chief Scientist at the British Geological Survey. He has done research in the Middle East and Asia, including highlights in Oman, Afghanistan, Saudi Arabia, Jordan, Pakistan, Iran, Israel and Iraq. He has honorary professorships at Nottingham and Leicester universities in the UK and is a visiting professor at the University of Milan, Italy and the University of Nanjing, China. He has published three books and over 100 peer-reviewed papers. His most recent book ‘Energy and Climate Change: An Introduction to Geological Controls, Interventions and Mitigations’ (Elsevier) examines the Earth system science context of the formation and use of fossil fuel resources, and the implications for climate change.

The cover image was provided by the British Geological Survey

Suggested further reading

Creamer, E, Eadson, W, van Veelen, B, et al. (2018). Community energy: Entanglements of community, state, and private sector. Geography Compass. https://doi.org/10.1111/gec3.12378

Bouzarovski, S, Haarstad, H. (2019).Rescaling low‐carbon transformations: Towards a relational ontology. Transactions of the Institute of British Geographers. 44: 256– 269. https://doi.org/10.1111/tran.12275